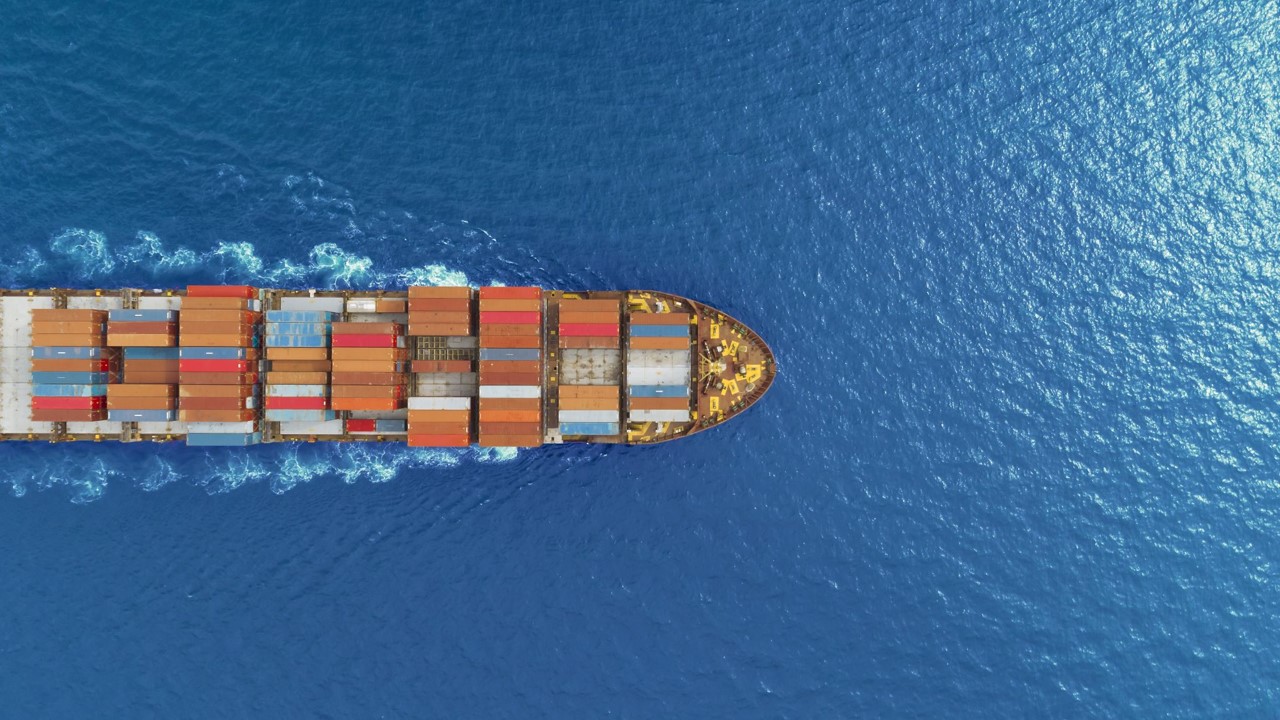

In its weekly World Container Index, supply chain advisory company Drewry has shown that the average cost of a 40-foot container is now more than four times higher than it was nine months ago.

Since April, the cost has gone from $2,706, to $5,901. To ship a container from China to North Europe – one of the busiest shipping trade lanes – has increased by 523 per cent vs last year. From China to the US west coast, the cost has increased by 320 per cent vs last year. And the to ship from China to the US east coast, the cost has gone up by 246 per cent.

These eyewatering numbers mean that the cost of relocating your goods now is so much more expensive than it was a year ago, albeit still significantly less than the previous pandemic peak. The average cost to ship a 40-foot container then was $10,377. But pre-pandemic? Well, the average cost was $1,420.

These are huge hikes in cost which are difficult to mitigate against.

But the pace of those increases, for the first time since early May, has slowed dramatically through July, with several consecutive weeks of small price decreases. So are the brakes finally being applied to rising costs? Or is this a slowdown before further acceleration? And what does it all mean for relocations?

What's caused prices to sky-rocket?

First, let’s take a look again at the causes behind these big price rises, which we have documented at length over the last seven or eight months.

Houthi attacks in the Red Sea

Many of the reasons for shipping’s cost increase woes can be charted back to the situation in the Red Sea.

When Houthi rebels first began attacking commercial vessels in the Red Sea late last year, costs soared as shipping lines scrambled to re-route vessels for obvious safety reasons.

The solution was to divert vessels transiting between Asia and the US east coast and Europe away from the Suez Canal and Red Sea, around southern Africa, past the Cape of Good Hope. This caused port scheduling challenges, and – given that the route is 3,500 nautical miles more and takes 10 days longer – forced shipping costs up significantly.

Then, as those schedules stabilized, prices began to fall in early February. Drewry’s World Container Index showed that prices fell from a peak of $3,964 in January, to $2,725 in early May.

But since then, the price incline has been dramatic. Further port congestion – particularly at major hubs like Singapore, constrained capacity on vessels and increased demand because of a better-than-predicted economic outlook in 2024 have all contributed to demand outstripping supply.

Record demand and shifting of the peak season

Xeneta has recently reported that demand for ocean freight shipping hit an all time record in May.

And, with the Red Sea conflict showing no signs of easing through autumn – when stock for Christmas is typically being moved around the world – there has been a move by retailers to both book slots for autumn long in advance and bring in whatever goods they can now.This means the “peak season” – which in shipping terms tends to last from mid-August through to mid-October, has been brought forward.

Do prices look like they might start to come down?

Mercifully, the answer to this is... maybe.

There has been some brighter news in recent weeks, which started with Drewry’s July 11 World Container Index showing that the average price rise had tumbled to just one per cent, a marked difference from the preceding weeks of double-digit price growth.

In the weeks since, we have seen tiny decreases to the price of slots on vessels.

Drewry has stated that it expects freight costs to “be high until the end of the peak season”, but is now of the view that prices may have peaked.

It is widely considered that the key resolution to this situation is ships beginning to use the Suez Canal again. But the chances of that – especially in the coming months – are very slim.

In addition, the other key in this context is to increase supply. This means reduced congestion at ports (and there are signs of this happening at big hubs like Singapore) and more capacity on ships. But in a recent blog, Emily Stausbøll of Xeneta, freight rate benchmarking and market analytics platform, said: “Severe port congestion in Singapore is now improving and continued delivery of new ships will add to available capacity. But congestion will take time to fully de-pressurize and has spread to other major ports.”

Advice and how we can help

As we continue to see supply chain volatility, driven by maritime incidents, we are advising our customers in the coming weeks or months to:

- Bake additional lead time into plans as far as possible – considering the peaks and troughs in supply and demand trends

- Budget for increased transport costs

As always, feel free to contact your move manager, and we can work through the challenges that this situation is presenting together.

If you're looking for a relocations, logistics or fine art company to help navigate these challenges as you look to make an international move, contact us by heading to the best suited brand page for your needs.